Skip to content

No results

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Search

Menu

Search

Artikel Trending

STPM Ulangan: Semakan Keputusan & Tarikh Peperiksaan 2024

Bantuan SARA 2024: Semakan Sumbangan Asas Rahmah STR

MyKasih: Semakan Sumbangan Asas Rahmah (SARa) STR 2024

Foodpanda Voucher April 2024: Jimat 40% Promo Codes Ini

Pendidikan

STPM Ulangan: Semakan Keputusan & Tarikh Peperiksaan 2024

Info

Tarikh Buka Sekolah KPM 2025

Zakat

Waktu Solat Aidil Adha & Bila Waktu Sesuai Untuk Bertakbir?

Kewangan

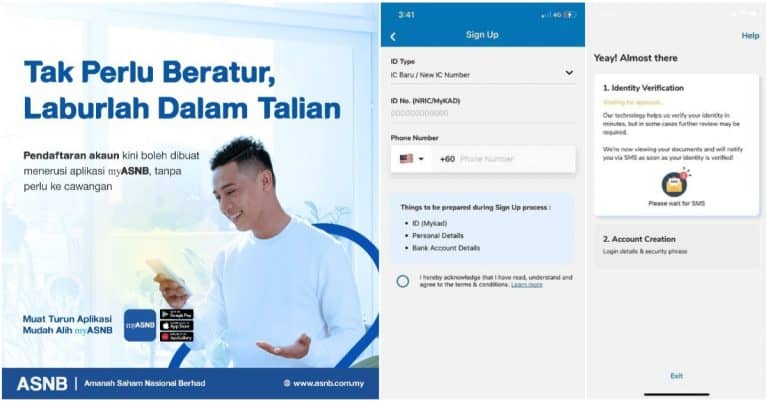

Cara Buka Akaun ASB Online Melalui Apps myASNB, Tak Perlu Ke Kaunter

Kewangan

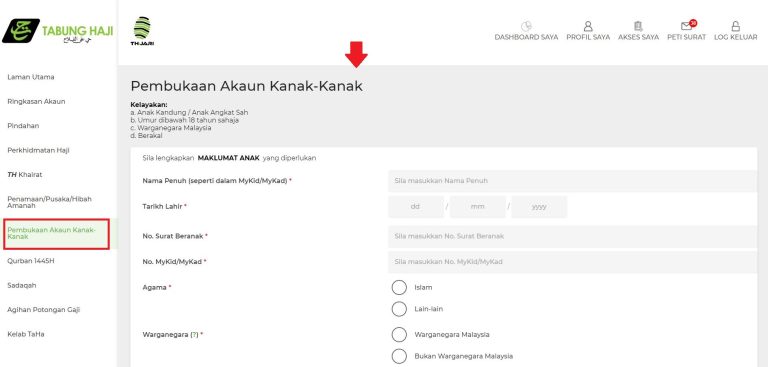

Cara Buka Akaun Tabung Haji (TH) Untuk Anak / Dewasa Online

Semakan

VIBES 2.0: Semakan Pencen & Bantuan Sara Hidup JHEV ATM

Contoh

Salam Subuh – Contoh Ucapan, Motivasi & Doa Pagi

1

2

3

4

…

308

Next

Load More

No more posts to load