Skip to content

No results

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Search

Menu

Search

Artikel Trending

Final Piala Thomas 2024 – [LIVE] Indonesia lwn China

Bantuan SARA 2024: Semakan Sumbangan Asas Rahmah STR

MyKasih: Semakan Sumbangan Asas Rahmah (SARa) STR 2024

Foodpanda Voucher April 2024: Jimat 40% Promo Codes Ini

Info

Final Piala Thomas 2024 – [LIVE] Indonesia lwn China

Info

Separuh Akhir Piala Thomas 2024 – [ LIVE ] Malaysia lwn China

Info

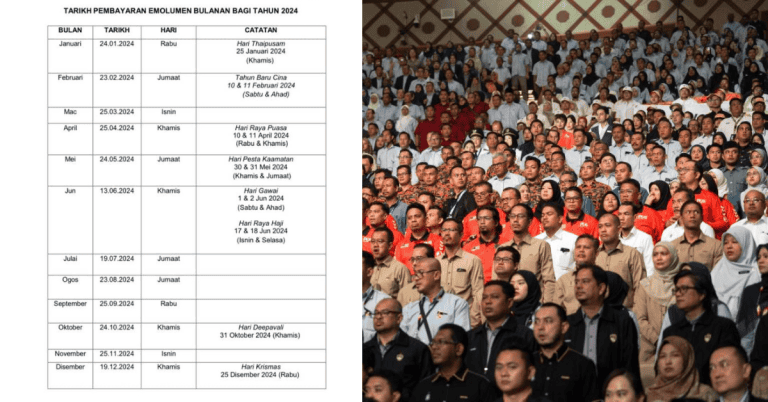

Gaji Mei 2024: Tarikh Pembayaran Gaji Penjawat Awam

Bantuan

Semakan Subsidi Tiket Penerbangan Pelajar IPT – Flysiswa (Fasa 2)

Info

Semakan

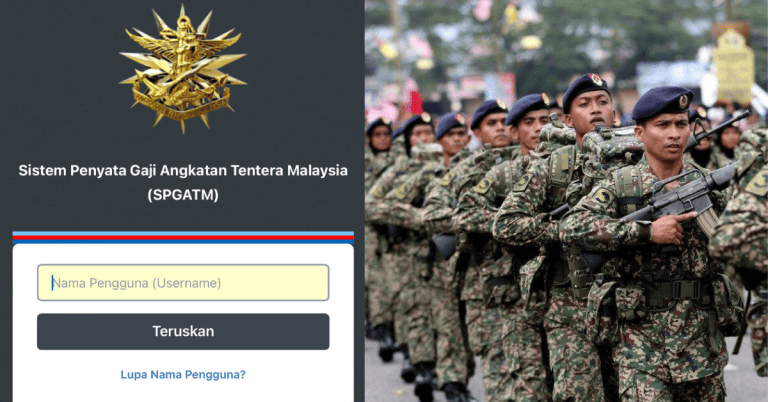

SPGATM: Semakan Penyata Gaji ATM

Info

Pendidikan

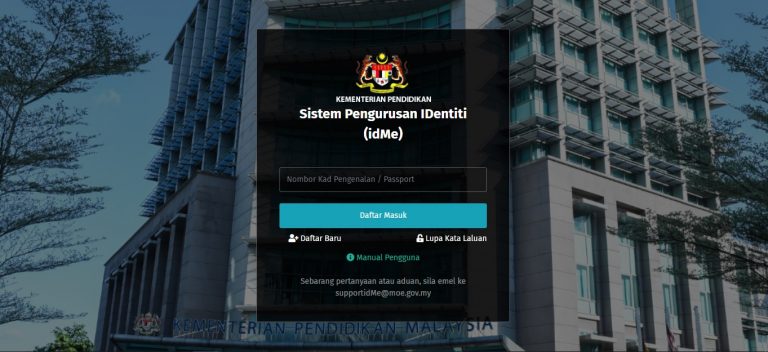

idMe KPM – Login Sistem Pendaftaran Tahun 1 KPM

Pendidikan

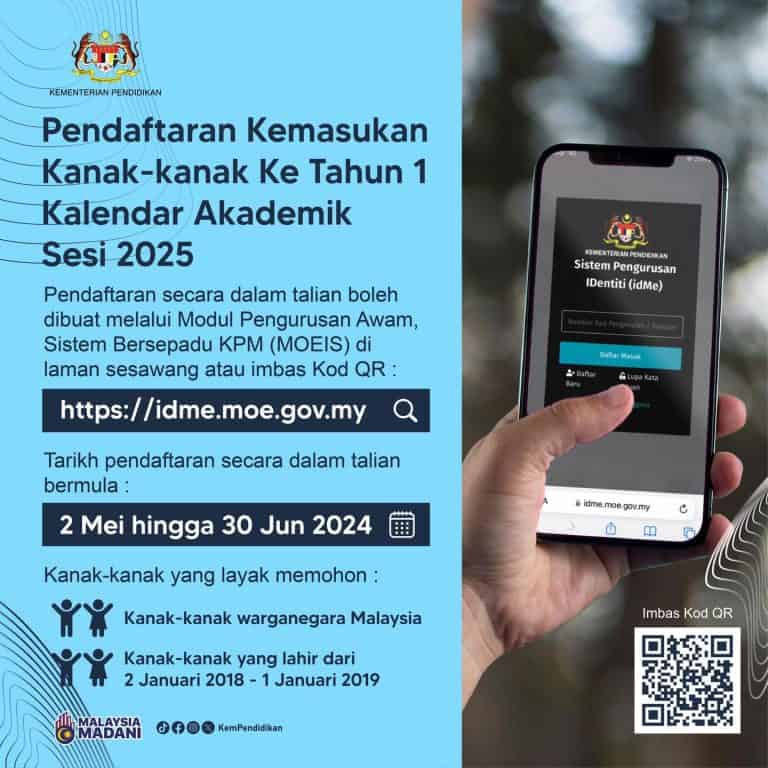

Pendaftaran Tahun 1 Sesi 2025 KPM (idme.moe.gov.my)

1

2

3

4

…

311

Next

Load More

No more posts to load