Skip to content

No results

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Kewangan

Bantuan

ASB

KWSP

Agama

Waktu Solat

Kesihatan

Teknologi

Login

APDM

Search

Menu

Search

Artikel Trending

Gaji Jun 2024: Tarikh Pembayaran Gaji Penjawat Awam

Kenaikan Gaji Penjawat Awam 15% Mulai Disember 2024

Pendaftaran Tahun 1 Sesi 2025 KPM (idme.moe.gov.my)

idMe KPM – Login Sistem Pendaftaran Tahun 1 KPM

Info

Gaji Jun 2024: Tarikh Pembayaran Gaji Penjawat Awam

Pendidikan

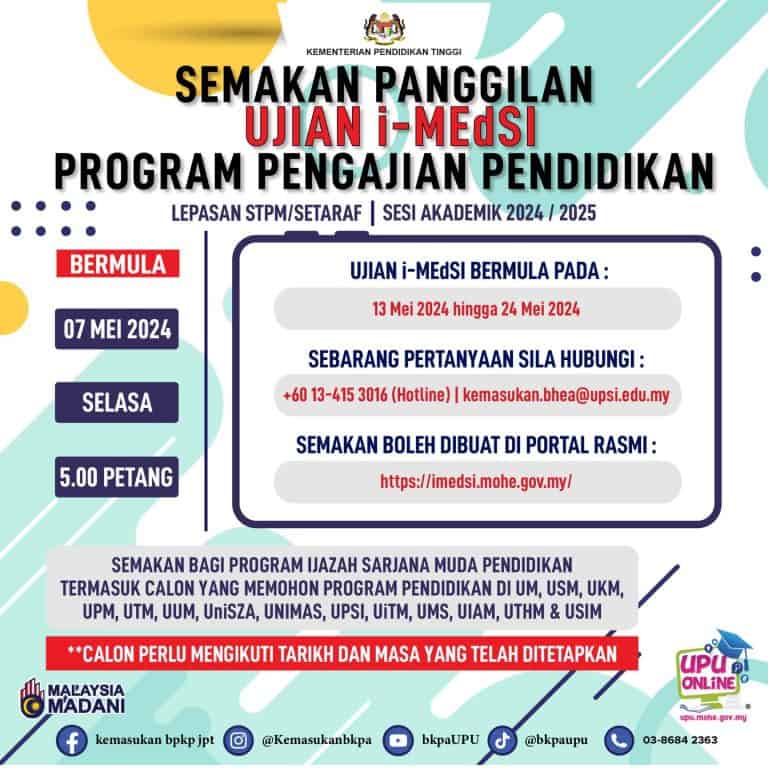

Ujian i-MEdSI Sesi 2024/2025 – Semakan Panggilan & Tips

Pendidikan

Hari Guru 2024: Tarikh & Sejarah Sambutan di Malaysia

Info

Ikan Bandaraya : Asal-Usul, Ciri-Ciri Unik dan Kesan Pada Ekosistem

KWSP

Pengeluaran KWSP 2024 : Jenis Akaun, Syarat & Cara Pengeluaran

Info

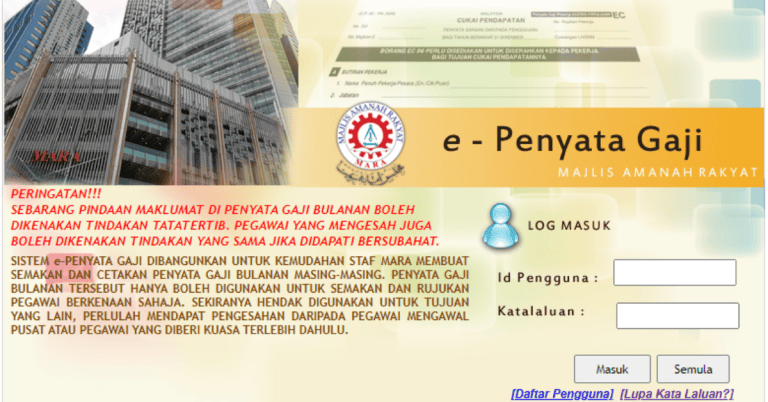

e-Penyata Gaji MARA: Semakan Penyata Gaji Kakitangan MARA

Pendidikan

Program Jom Baca: Objektif & Pelaksanaan Program

1

2

3

4

…

311

Next

Load More

No more posts to load